Walk into any kitchen on the planet and you’ll find it somewhere in the tea, the biscuits, the morning cereal. Sugar is one of those quiet commodities that nobody thinks about until the price moves, and when it does, entire economies feel the jolt. Behind every spoonful sits a sprawling global trade network worth tens of billions of dollars a year, where a handful of countries effectively decide how sweet the rest of the world gets to be.

If you’ve ever wondered who actually controls that flow, the answer lives inside the sugar export data that trade analysts pore over every season.

This post breaks down the heavy hitters the countries that ship the most sugar across borders, why they dominate, and what the latest numbers reveal about where the market is heading.

Why Sugar Export Data Matters More Than You’d Think

Sugar isn’t just a pantry staple; it’s a strategic agricultural asset. Roughly 80% of the world’s sugar comes from sugarcane grown in tropical zones, with the remaining share drawn from sugar beet farmed in cooler temperate regions. That split alone shapes who can produce a surplus and who has to import. When a major producer has a bumper harvest, global prices soften. When drought hits a key region, the ripple effect reaches grocery shelves thousands of miles away.

Traders, manufacturers, and policymakers lean on sugar export data to make calls that involve serious money. A confectionery giant locking in supply contracts, a government deciding whether to allow exports, an investor betting on commodity futures all of them are reading the same tea leaves. The total value of global sugar exports reached roughly $70.6 billion in 2024, moving around 68 million metric tons across borders. Those are not small stakes.

A few reasons this data is worth tracking closely:

- Price forecasting– Export volumes from top suppliers directly influence world raw and refined sugar prices.

- Supply security– Importing nations watch exporter harvests to plan their own food reserves.

- Policy decisions– Governments use the numbers to set export quotas, duties, and subsidies.

- Trade strategy– Businesses identify reliable sourcing partners and hedge against disruption.

Brazil: The Undisputed Top Sugar Exporter

If there’s one name that dominates every conversation about the World largest exporter of sugar, it’s Brazil. The country sits in a class of its own, shipping out far more than any rival and effectively setting the tempo for the entire global market. Brazil’s record output alone accounts for close to a quarter of global supply, which is why a single weather event in its cane belt can swing prices worldwide.

What gives Brazil its edge is a combination of vast arable land, a favourable climate, and a flexible production system that lets mills shift their cane between sugar and ethanol depending on which is more profitable. In the 2024/25 marketing year, Brazil exported roughly 35.8 million metric tons of sugar, dwarfing the field. With production forecast to climb toward a record 44.7 million tons in 2025/26, its grip on the title shows no sign of loosening.

- Largest cane producer and exporter, by a wide margin

- Flexible sugar-versus-ethanol production keeps it competitive across price cycles

- Strong port infrastructure built specifically for bulk commodity export

The Rest of the Top Five: Thailand, India, Australia and Guatemala

Below Brazil, the rankings get more interesting and more volatile, because the next tier swings with monsoons, government policy, and shifting domestic demand. Thailand has reclaimed its footing as the world’s second-largest exporter after recovering from a brutal drought, with its cane crop rebounding sharply. India, despite being the planet’s biggest consumer and one of its largest producers, is a wild card its export volumes rise and fall dramatically depending on government permissions and harvest size.

Australia and Guatemala round out the upper ranks as smaller but remarkably consistent suppliers. Australia’s efficient, export-oriented industry and Guatemala’s competitive Central American operations keep both firmly in the conversation. Anyone studying sugar export quickly learns that the order below Brazil is never fixed for long.

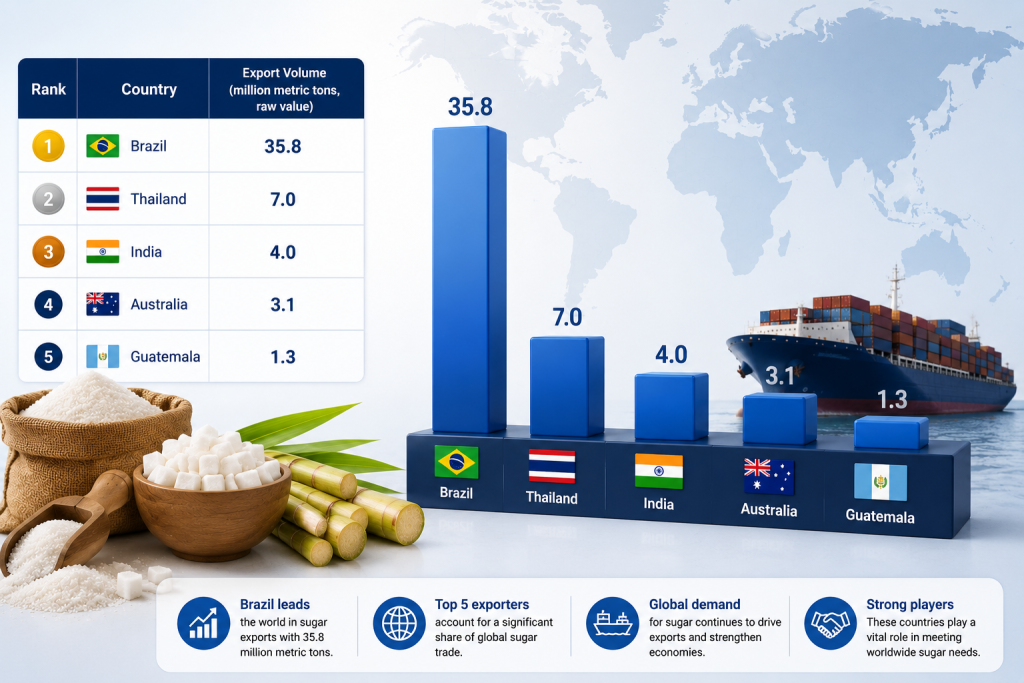

Here’s how the leading exporters stacked up in the 2024/25 marketing year, based on USDA figures:

| Rank | Country | Export Volume (million metric tons, raw value) |

|---|---|---|

| 1 | Brazil | 35.8 |

| 2 | Thailand | 7.0 |

| 3 | India | 4.0 |

| 4 | Australia | 3.1 |

| 5 | Guatemala | 1.3 |

What’s Driving the Shifts in Sugar Trade

The hierarchy of the top sugar exporter nations isn’t carved in stone — it bends to forces that are partly natural and partly political. Weather remains the single biggest variable. A strong monsoon in India or steady rainfall in Thailand can add millions of tons to global availability, while drought in Brazil’s interior tightens supply almost overnight. Layered on top of that is government policy: India in particular treats sugar exports as a lever, opening and closing the tap based on domestic stocks and food-security concerns.

Production costs also separate the winners from the strugglers. Brazil and Thailand enjoy some of the lowest raw sugar production costs in the world, while the European Union a net player with higher beet-processing costs operates on much thinner margins. These cost gaps explain why low-cost producers can keep exporting profitably even when world prices dip.

The table below illustrates how production economics vary across key regions, a factor that ultimately feeds into who can compete on the export stage:

| Region | Approx. Raw Sugar Production Cost (USD per metric ton) | Competitive Position |

|---|---|---|

| Thailand | ~458 | Highly competitive |

| India | ~470 | Competitive, policy-dependent |

| European Union | 700+ | High-cost, margin-sensitive |

How to Read and Use Sugar Export Data Wisely

Numbers are only useful if you know how to interpret them. The first thing to understand is the difference between “raw value” and refined figures most global reporting, including the widely cited USDA data, expresses volumes in raw value to allow apples-to-apples comparison. Marketing years also differ by country; Brazil runs April to March, Thailand December to November, which means a headline figure for one season may not align neatly with another’s calendar.

When you’re evaluating a supplier or a market trend, look beyond a single year’s snapshot. A country’s export volume can crater in one season due to a policy freeze and bounce back the next. Tracking multi-year trends, watching production forecasts, and noting the sugar-versus-ethanol split in places like Brazil will tell you far more than any one data point ever could.

- Check whether figures are raw value or refined before comparing

- Account for differing national marketing years

- Watch production forecasts, not just past exports, for forward signals

- Factor in policy risk for politically managed exporters like India

Read This Blog Also- Top 10 Biggest Food Exporters in the World

The Bottom Line

The global sugar trade is a story of a few dominant players and a constantly shifting supporting cast. Brazil reigns supreme and likely will for the foreseeable future, but the countries jostling beneath it keep the market lively and unpredictable. For traders, manufacturers, and curious observers alike, staying current on reliable sugar hs code is the difference between reacting to the market and anticipating it.

For those who want deeper, well-organised insights into global commodity trade and business intelligence, Vyaapar One brings together the kind of clear, accessible analysis that turns raw numbers into decisions you can act on with confidence.